I am calling PWL Capital honcho Cameron Passmore "renegade" because I don't want to antagonize someone I find respectable. But it turns out, the dictionary defines "renegade" as a person who betrays a faith or a cause. Well, the meaning of words changes through usage, I think the dictionary is wrong. Today, renegade means "unorthodox" or "maverick." Source: me. PWL Capital - famous for having Shopify moguls Tobi Lütke and Harley Finkelstein’s endorsement - requires me to coin a new term. They are "closet non-indexers." They preach the virtues of indexing but primarily put clients in funds trying to outsmart indexes. PWL’s active bets on cheaper, smaller companies have to date detracted from what clients could have achieved via mainstream indexing. This is the result of the “value” strategy going through an unprecedented, decade-plus dry spell. And small caps generally underperforming large caps over that timeframe. The opportunity cost to clients is noticeable, though not as big as I would have initially thought. The Globe and Mail has said of PWL’s Executive Chairman Cameron Passmore, that he promises one thing: “passive index investing for ultra-low fees.” Let's apply some good old forensic kompromatology to that claim.

PWL’s growth from sleepy to “rock-star” status

PWL Capital has high growth, billions in assets under management and offices in Montreal, Ottawa and Toronto. PWL was founded in Montreal in 1996 and was a pretty sleepy firm with a very retirement-oriented practice. But then, in the past decade, AUM growth has been turbo-charged, roughly as follows:

2015: $1.1B

2016: $1.3B

2019: $2.7B

2021: $4B

2024: $4.4B

The main engine of this growth is Ottawa-based PWL advisor Cameron Passmore. He struck gold by connecting with Shopify founder Tobi Lütke in 2011. Tobi doesn’t like the Big Canadian banks (as you can see from his stingy allotment to them when his company raises money.) Tobi fell for Passmore’s “non-sales-y” pitch and in turn opened the doors of Shopify, allowing him to pitch PWL’s wares from within the tech company’s offices. Fellow Shopify biggie Harley Finkelstein along with scores of other Shopifolk also became clients. Given the density of newly minted millionaires at Shopify and Ottawa’s tech community, this turbo-charged the growth of Passmore’s book. He more than quadrupled his assets to $450m within five years of meeting Tobi. By 2016, more than 100 Shopifolk entrusted their money to Passmore, representing more than half his book. To quote one client: “If it’s good enough for Tobi, it’s good enough for me.”

There are actually 3 other advisor teams at PWL, besides Passmore. Passmore’s team is now known as “PWL Capital” - he is PWL. This was inevitable as Cameron Passmore was the rainmaker who had accounted for the bulk of the growth. The arrangement with the other advisor teams is that they are independents, sharing PWL’s platform. Passmore has thus eclipsed the three titular founders of PWL: James Parkyn is with one of the “other teams.” Laurent Wermenlinger left for Desjardins in 2006. Anthony Layton retired and sold his majority stake in the firm to Passmore in 2021. They branded this a “100-year-vision” and a multi-generation succession plan.

How did Tobi become a client? He was traumatized by his family’s history of bad investing and so he did a lot of research to avoid their fate. He eventually asked Ottawa-based blogger Ram Balakrishnan for a referral. Ram was an active blogger about personal finance matters, who advocated passive investing. This is not to be confused with an haute finance blogger like me. But still, I think Ram can justifiably take credit for having been the catalyst to building a billion-dollar wealth management firm.

Tobi and the Shopifolk’s association with PWL was reported in 2016 by Sean Silcoff in the Globe and Mail. In a hagiographic profile of Passmore titled: “Invest like a tech gazillionaire.” Never mind Tobi, you can imagine what a calling card it must be that Sean Silcoff will even look at you. More than look, Silcoff might have had visions, writing that Passmore had reached “rock-star” status.

Passmore confirmed to the Ottawa Business Journal in 2021 that Shopify clients still make up “a significant part” of his client base. And that Finkelstein was still a client. Tobi’s status as a current client is unclear. His Shopify wealth has grown exponentially since he started as a client of PWL in 2011. He also now has an investment office, Snowdevil Capital. If I had to bet, I would say Tobi is probably no longer a meaningful PWL client. At his scale, it makes no sense to have an external passive manager. Plus, PWL is no longer willing to confirm that he’s a client, that’s a clue. Here are some PWL clients among the Shopifolk who were part of the photo in the Silcoff article, at Shopify’s offices.

This photo, along with the glamour shot below of Passmore in a state of partial undress, were taken at Shopify headquarters. I should warn you that this photo is suggestive if you are a sock fetishist. In Silcoff’s defence, I don’t think journalists dictate the artistic direction of the photos.

Just before we get to polemics, I feel it’s important to say that unlike many other firms I have analyzed, I do not detect a pattern at PWL where the firm is set up top-to-bottom to exploit clients. I respect Passmore and his close associate, Head of Research and YouTube celebrity, Ben Felix. The latter produces a lot of content and I consider what he writes to be a reference. I had the chance to talk to Ben Felix as part of writing this. Just his willingness to talk openly, knowing that I’m a critic, shows that the firm operates in good faith. I would rate the firm an 8 out of 10. This easily puts the firm in the top 10% of all Canadian money managers. I bumped up the score because I expect their strategy will rebound. While I will still devote several paragraphs to my usual schadenfreude leitmotif, I think the bigger take-away should be that the long-awaited, near-mythical, value renaissance might already be under-way. Indeed, over the past 3 years, PWL has outperformed its benchmarks.

I can’t believe it’s not beta!

One of the strands of Silcoff’s article is that tech people are data-driven and the data shows most active managers don’t beat the index. Silcoff writes about Passmore:

He doesn't offer exclusive access to sophisticated, exotic investment vehicles or funnel cash to star fund managers renowned for generating outsized returns. Rather, Passmore promises one thing: passive index investing for ultra-low fees.

In total, the words “index” and “indexing” appear 15 times in Silcoff’s article. This sort of mistaken impression floating around PWL is well captured by this post from a Reddit user from a few months ago (which I have edited for clarity):

There is seemingly something at odds from what I can tell…. How come PWL Capital preach about ETF and index investing while also running what I understand to be an active fund? The podcast in particular reiterates over and over how large ETFs and index funds (VEQT, S&P500 index tracking ETFs, etc) outperform the vast majority of active fund managers in the long term. Is PWL Capital also not at least in part an active fund?

I am not too interested in the active vs passive classification as I think that’s pretty murky - even the S&P 500 can be considered active management. In my view, passive vs active should be thought of as a spectrum. But I am more interested in whether PWL indexes, which is a more binary question. It should also be clarified that PWL doesn’t run its own fund as the poster claims. Rather, it uses multiple funds from a large American manager, Dimensional. Passmore's team - in the main - invest client money in Dimensional funds. Some background about Dimensional: they are a giant Texas-based fund shop - not quite as gigantic as Blackrock or Vanguard, but in that vicinity. They are in the top 15 by size.

It doesn’t take much research to realize that the Passmore team is not primarily engaged in indexing. For the simple reason that Dimensional is not engaged in indexing. Dimensional uses the tag line “Going beyond indexing since 1981” right on their website’s homepage. That’s a pretty good clue. Beyond Indexing is like “Beyond Meat” - it’s not meat.

Consider the extent to which Dimensional goes to profess their superiority to indexing in this video titled “You can do better than indexing.”

Other Dimensional indexing-bashing YouTube videos you can look up include “Dimensional looks at rebalancing every day. Indexers can’t.” and “Advantages over an index-tracking fund.”

Passmore’s claim to be engaged in indexing is a fantasy on the level of meat-based vegetables. In my view, either you are indexing or you are trying to outsmart the index. The essence of indexing is to come up with a judgment-free representation of the broad stock market. The minute you come up with notions like “value” or that profitable firms should outperform, you are no longer indexing. Any knowledgeable investment professional would understand that Dimensional is engaged in “factor investing” or so-called “smart beta”, or “systematic investing”, not indexing.

Dimensional founder David Booth clears up the issue, saying in a corporate video:

“Dimensional built the firm on the idea that we could do better than indexing. And that’s the way to evaluate us, I think. You know, do we do better than index funds or not?”

Dan Bortolotti, now a PWL advisor, writes in a 2012 review of Dimensional Fund Advisors on his blog (prior to joining PWL):

“They’re not index funds, and it’s not even accurate to say they’re passively managed, though there is certainly no stock selection, timing, or forecasting involved.”

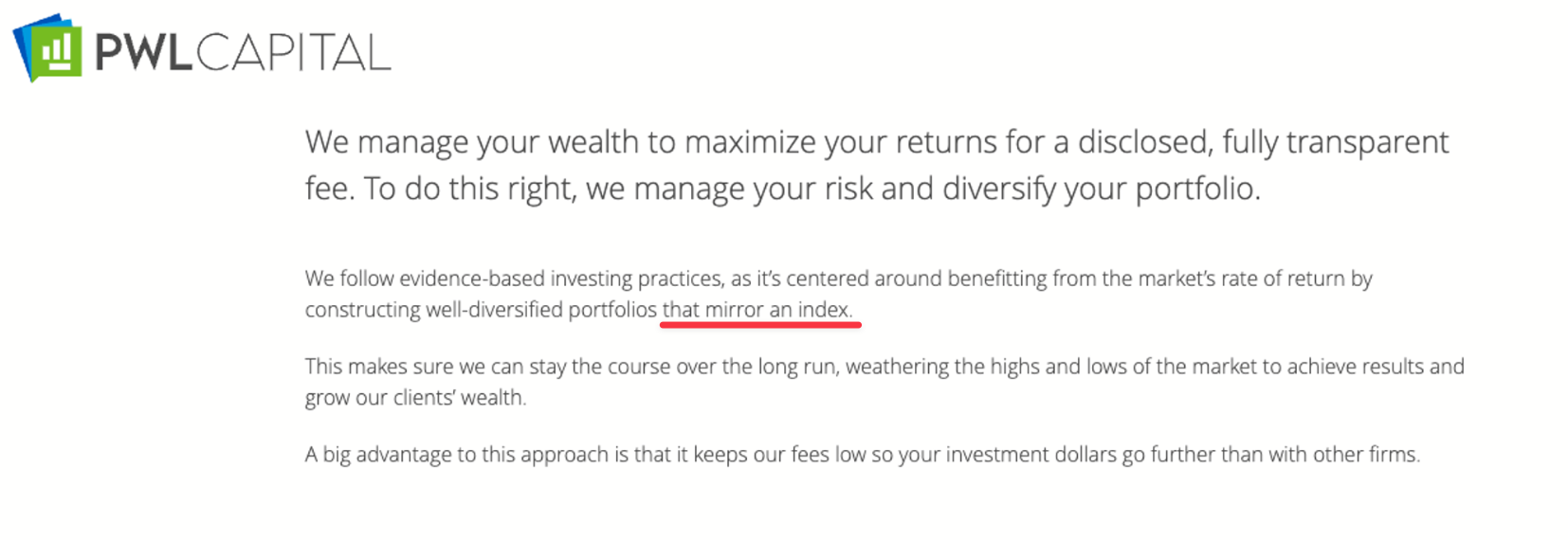

And yet, until a few days ago, PWL said on the section of its website describing its portfolio management:

We follow evidence-based investing practices, as it’s centered around benefitting from the market’s rate of return by constructing well-diversified portfolios that mirror an index. This excerpt can be seen in the screenshot below:

Within hours of my discussion with PWL’s Ben Felix, he confirmed to me that the language has been changed to eliminate the notion of mirroring an index. I take this as a sign that they are committed to doing the right thing. The Silcoff article does mention Dimensional in one paragraph and mentions the “tilting” to smaller, cheaper stocks. But it identifies Dimensional as an “index fund company”, which is clearly wrong. And the thrust of the article is about the triumph of indexing and how finance luminaries like Warren Buffett, Burton Malkiel and John Bogle approve of it.

There was a Globe article in January called “Canadians are bananas for not embracing index funds.” Guess who’s quoted? PWL has captured enormous indexing mindshare. In the very first episode of the popular PWL podcast, Rational Reminder, they say, by way of introducing the firm: “For our clients, we recommend index funds in general and index funds from a company called DFA - Dimensional Fund Advisors.” The second episode is titled “Index investing is here to stay.” Passmore says in that Silcoff article: “All the evidence points toward indexing.” If that’s the case, why is he selling Dimensional products?

Indexing has been widely endorsed by knowledgeable people, everyone from your savvy uncle to Warren Buffett. Does PWL’s marketing seek to bask in the glow of the indexing revolution, despite PWL not being a genuine indexer? The sinister interpretation would be that at some point, it was easier to hitch PWL’s wagon to the indexing freight train than to pitch something more accurate, but more technical and obscure like “factor tilting.” The more benign explanation could be that PWL saw the use of “indexing” as a harmless simplification. I am not a mind-reader, but I lean towards giving PWL the benefit of the doubt and would call this a “communication blunder” that is now in the past.

PWL seems to have conceded the point, though I think deep down, they view indexing as non-binary. One concession I would make is that indexing by itself is no panacea. I would say Dimensional is obviously closer in spirit to indexing, than say, an ETF based on an index of uranium stocks. Indexing advocates should use the term "broad market indexing" to avoid such confusion. Also, while Passmore is a strong proponent of Dimensional, other teams at PWL do incorporate plain vanilla index funds more significantly. One heavyweight in PWL's corner is the SEC. In 2018, they issued an advisory on "non-traditional index funds." Under that label, they lumped together smart beta, quant and ESG funds. So the SEC classifies smart beta as index funds, albeit with the "non-traditional" qualifier. Fortunately, there's a simple way to reconcile this seeming contradiction: the SEC is completely wrong.

In any event, far more consequential, is that in my capacity as Bay Street's Chief Kompromat Officer, I totally pardon PWL on this imbroglio. Or brouhaha, if you prefer. Or kerfuffle. You can always trust me, because I know all the best words and precisely what they mean. In another post later on, I will analyze PWL’s performance and fees.