To be clear, I don't agree with the law I bring up in this post at all. I am simply reporting the fact that violations are a dime a dozen. If Wealthsimple trips over them, you can imagine how easy it is for smaller players to be offside.

So Wealthsimple is offering financial planning services in Quebec without the appropriate license. Quebec is fairly unique in requiring anyone offering financial planning services to hold a license issued by the financial regulator. I have checked and Wealthsimple does not hold this particular license with Quebec's securities regulator.

Most professional licensing laws make it an offence both to advertise services for which you don't have a license (generally termed "holding out") as well as actually perform the service. This is the case for financial planning in Quebec. (In contrast, Ontario regulates the use of the "financial planner" title, but not the actual performance of financial planning.) It's easy for me to confirm, at a minimum, that Wealthsimple is violating the "holding out" provision. I live in Quebec, so I should not be able to see this:

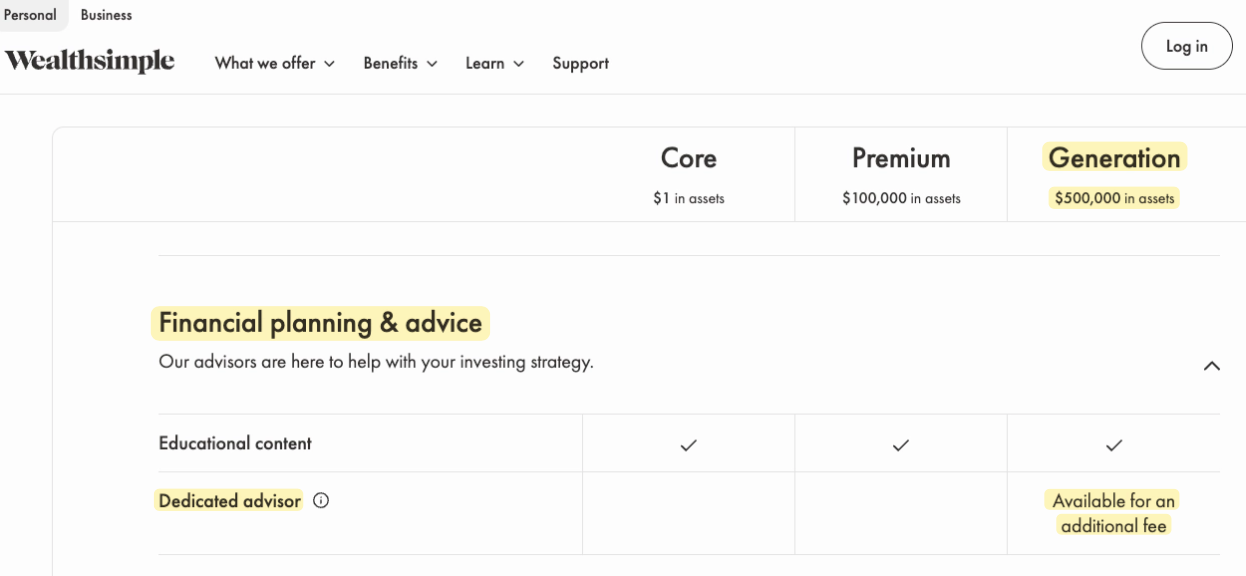

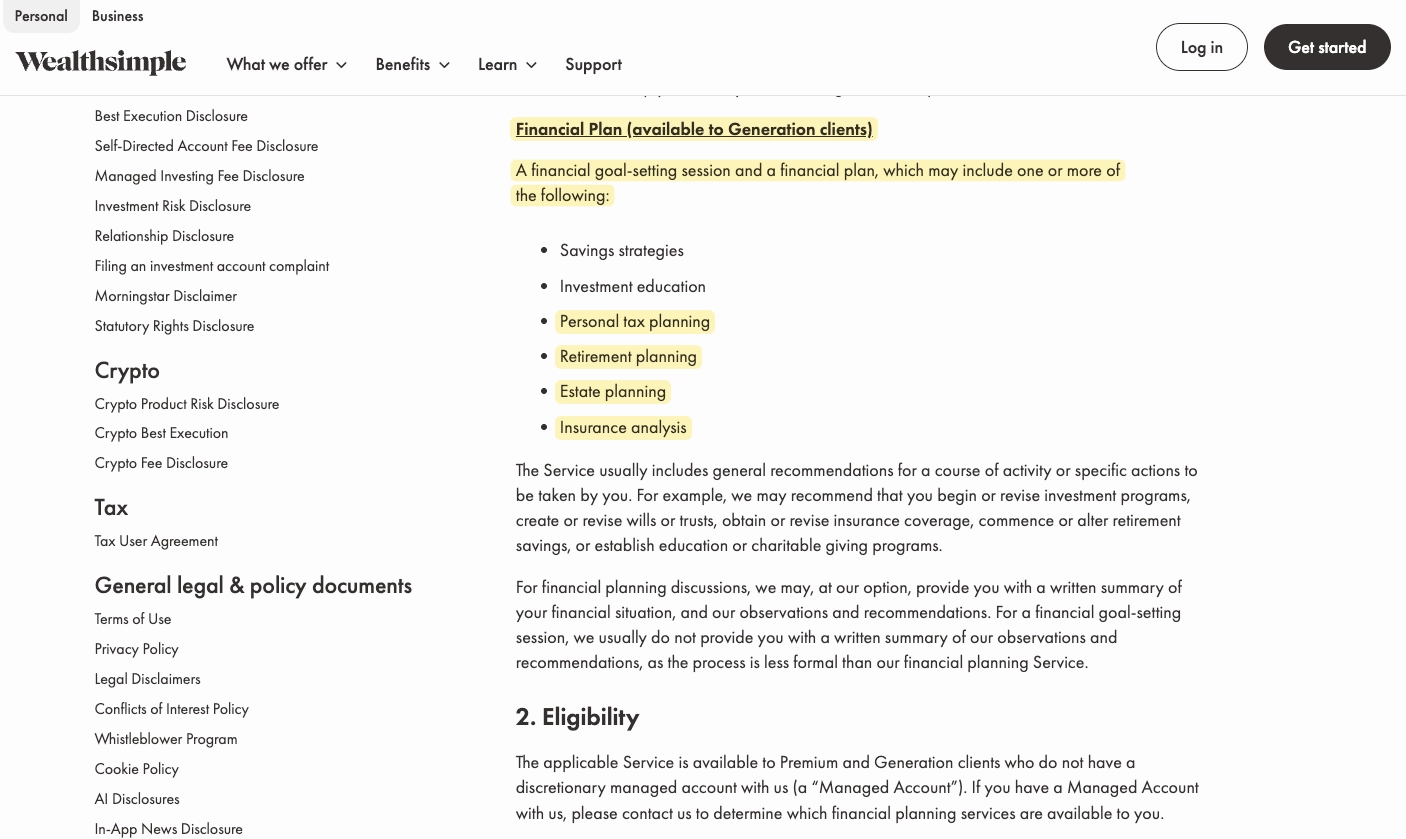

Wealthsimple specifically advertizes personalized financial planning from a dedicated advisor as a perk for "Generation" clients (ie. those having more than $500k). Clients pay an extra fee for this, starting at 0.4% for clients with portfolios under $1m. Under contract law, an unlawful provision (such as providing unlicensed financial planning) may void the agreement in whole or in part.

In Quebec, this aspect of contract law is made explicit in the Civil Code. And so if any Quebec clients got (unlicensed) financial planning, they may have legal recourses to recover some of their fees. I shared my conclusions with Wealthsimple's crypto-loving Chief Legal Officer Blair Wiley on Thursday February 26th. He did not respond.

Quebec's Financial Markets Authority took part in last year's Declaration of War Against Finfluencers. Regulators want to go after finfluencers who may violate licensing requirements. Finfluencers could be based anywhere in the world. Yet a $100B giant flouts licensing laws right under their nose.

One perfectly reasonable question is how can a licensed portfolio manager in Quebec (as Wealthsimple is) manage wealth without engaging in at least minimal financial planning? After all, money managers have know-your-client and suitability obligations, which require considering the financial circumstances of the client. Well, these are some of the great paradoxes of securities regulation, more vexing than Schrödinger’s cat. As I said, I don't agree with the law.

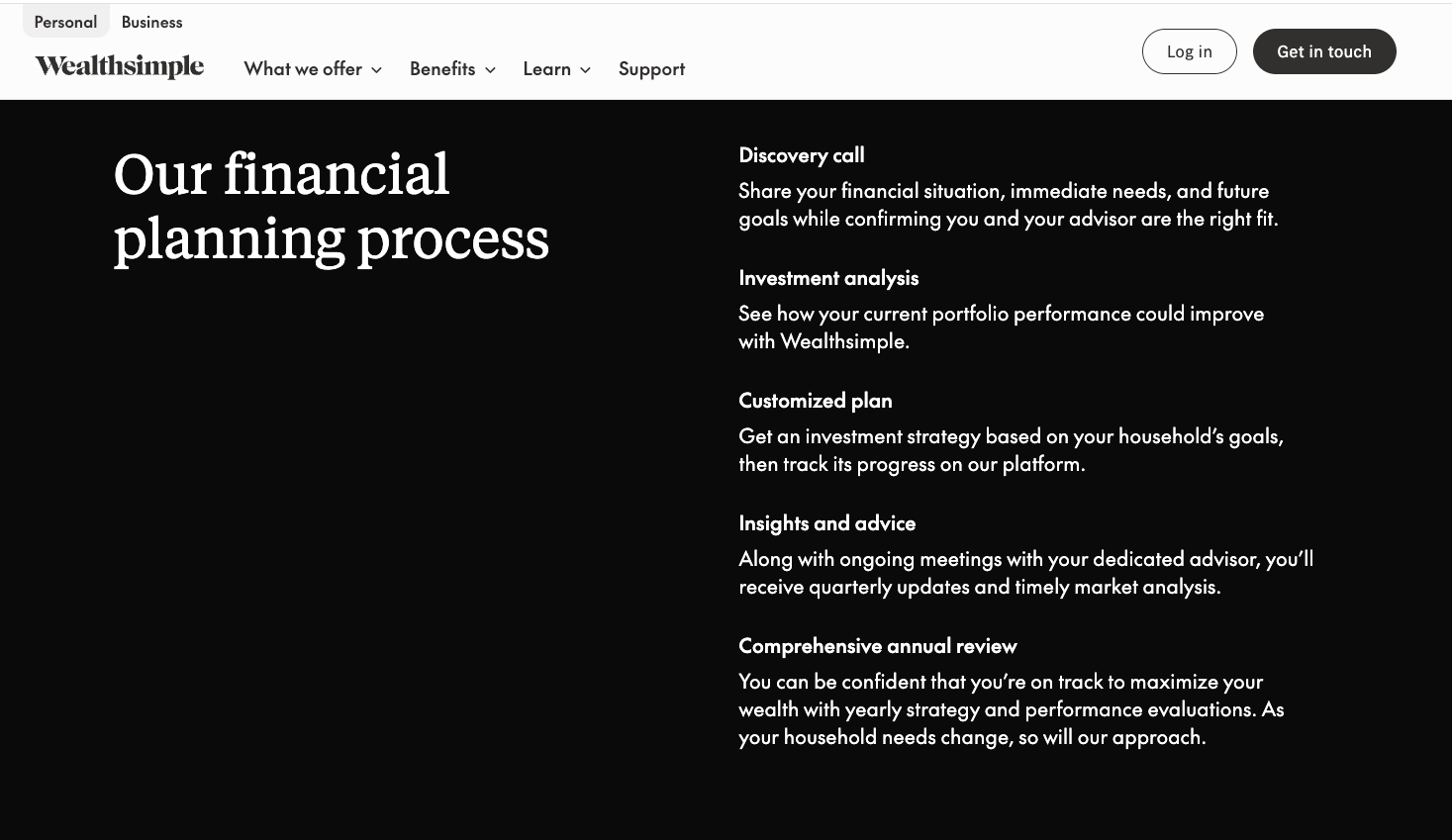

Portfolio managers who are not dually-licensed in Quebec must navigate this carefully. In my view, Wealthsimple has strayed too far into advertising financial planning in Quebec, as you can see from this itemized list they provide. (Again, relevant to the “holding out” provision.)

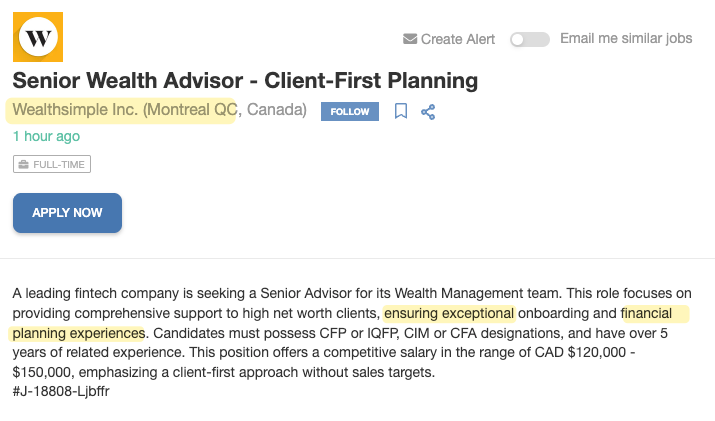

As I have myself never experienced the wonders of Wealthsimple’s wealth management, I do not know if they have actually done financial planning for Quebec clients. But that seems likely from the lack of any Quebec carve-out language in their legal terms. Here they are recruiting for someone to offer "financial planning experiences" in Montreal.

Any human financial planner who provides financial planning from Quebec or to Quebec clients must be licensed in their personal capacity as well. This might sound harsh, but they might be more culpable if they failed to inform their employer of the regulated nature of their life's calling in the province they call home.

Here's one "wealth management leader" at Wealthsimple, who uses the protected "Pl. Fin." title (the French abbreviation of financial planner) without holding the appropriate certificate from the Quebec regulator. That by itself is an offence.